On April 1, you will post a debit entry to the rent receivable account for $800 and post a corresponding credit entry to the rental revenue account for the same amount. However, once you receive the rental payment, you decrease the rent receivable account with an $800 credit entry and post a debit entry for the same amount to the company’s cash account. Under both accounting standards, we are recording a cash payment of $100,000 and total lease expense of $115,639. Under ASC 842 periodic lease expense is made up of the periodic interest and asset depreciation shown in columns “liability lease expense” and “asset lease expense,” respectively. Although the deferred rent account used under ASC 840 is eliminated under ASC 842, the difference between the straight-line rent expense and the cash paid is still reflected on a company’s books. Under ASC 842, the net activity in the lease liability and ROU asset accounts each month is essentially deferred rent.

Accruing Rental Income

The total liability balance (short-term and long-term liability balances) is often used by stakeholders to evaluate whether to invest or lend to an organization. Potential investors or lenders use those balances in financial ratios that often greatly contribute to decision-making. Organization’s lease activity is more transparent, which was ultimately the goal of the FASB’s issuance of a new lease accounting standard. On the 10th of March, Unreal Corporation received rent 20,000 via a cheque from tenant ABC for one of its property on rent. Show related journal entries for office rent received in the books of Unreal Corporation.

What is rent expense?

Step 2 – Transferring office rent expense into income statement (profit and loss account). Another sophisticated method involves integrating artificial intelligence (AI) into the receivables management process. AI-driven chatbots can handle routine tenant inquiries about rent payments, freeing up human resources for more complex tasks. These chatbots can also send automated reminders and follow-ups, ensuring that tenants are consistently aware of their payment obligations. Additionally, AI can analyze historical data to recommend optimal times for sending payment reminders, maximizing the likelihood of timely payments. Effective management of rent receivables is crucial for maintaining the financial health of any property management or real estate business.

Example: Straight-line rent expense calculation

- This process not only aids in maintaining transparent records but also supports effective financial management and decision-making.

- The entry the lessee makes at the beginning of the lease agreement under ASC 842 is to record the initial ROU asset and lease liability.

- The accrued rent receivable account is considered a current asset, since rent is typically due within the next year.

- Under both ASC 840 and ASC 842, the formula to calculate straight-line rent expense is total net lease payments divided by the total number of periods in the lease.

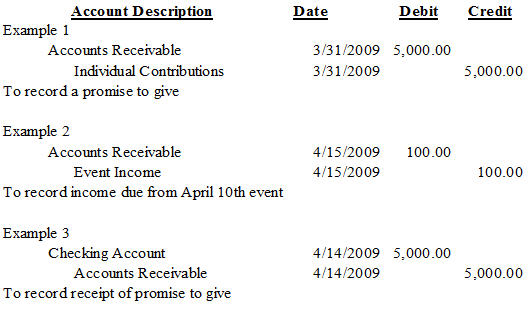

- We need to replace the Debtors with Rent Receivable on the debit side of the Journal entry and Sales revenue with Rental revenue on the credit side of the Journal entry.

Conversely, if deferred rent has a debit balance at transition, a credit to deferred rent and an offsetting debit to the ROU asset will be recorded. Since the rent expense is an average, there will be months where rent receivable journal entry cash is more than the straight-line expense and correspondingly months where cash is less than the expense. Deferred rent occurs in periods where the expense incurred is greater than cash paid for rent.

Differences in timing of cash flows in rent payments

Rent revenue, on the other hand, is an income statement account that indicates rent earned during a specified period of time. The distinction between rent receivable and rent revenue accounts is important to note for proper accounting purposes. When the tenant makes a payment, the landlord reverses the journal entry and credits the Cash account and debits the Rent Receivable account. If this journal entry is not made, the total assets on the balance sheet and total revenue on the income statement will be understated by $5,000 in January 2021. If this journal entry is not made, both total assets on the balance sheet and total revenue on the income statement will be understated. This situation is recorded with a credit to a liability called Accrued Rent, representing the obligation to pay at a later date for the benefit received.

Advanced techniques can significantly enhance the efficiency and reliability of receivables management, ultimately improving financial stability. By leveraging data analytics tools, property managers can forecast tenant payment behaviors and identify patterns that may indicate future delinquencies. This proactive approach allows for early intervention, such as personalized payment plans or targeted communication strategies, to address potential issues before they become problematic. In addition to recording receivables, it’s important to account for potential bad debts. This allowance is an estimate of the receivables that may not be collected and is recorded as a contra-asset account, reducing the total receivables on the balance sheet. This practice aligns with the conservatism principle in accounting, ensuring that assets are not overstated.

The party receiving the rent may book a journal entry for the rent received. When cash payments in a period were less than the expense incurred, deferred rent would be recognized on the balance sheet as a credit balance. This was considered a deferral, which is a liability, as expense for rent was incurred, but some of the amount was still owed. For further explanation of deferred rent, see our blog, Deferred Rent under ASC 842 Explained with Examples and Journal Entries. However, the presence of significant rent receivables can also signal potential issues.

The act of recognizing the expense when the company is obligated to pay for the use of the asset but before payment is made is called accruing the expense. Whenever the rent is paid, the accrued rent will be reduced by the amount paid. Accrued rent receivable is the amount of rent that a landlord has earned, but for which payment from the tenant is still outstanding. This situation arises when a tenant has made use of property owned by the landlord, but has not yet paid the agreed-upon amount of rent for that usage period. This entry is made as part of the closing process at the end of each reporting period. Per ASC 842, the ROU asset is equal to the lease liability calculated in step 3 above, adjusted by deferred or prepaid rent and lease incentives.

Rent revenue, on the other hand, is an income statement account and is reported over the course of the period. In this case, at the period adjusting entry of January 31, 2021, the company ABC needs to make the journal entry for accrued rent revenue that it has earned in January 2021 for the office space rental fee. A similar adjustment will be made for any deferred rent expense at the transition to ASC 842. If deferred rent has a credit balance, the balance will be cleared with a debit and the offsetting credit will be recorded to the appropriate ROU asset.

The accrued rent receivable account is considered a current asset, since rent is typically due within the next year. A landlord could offset this receivable with an allowance for doubtful accounts, if there is a probability that a tenant will not pay rent. Show related journal entries for office rent paid in the books of Unreal Corporation.